.png)

US strikes on Iran escalate tensions, oil surges, and the Strait of Hormuz becomes the market’s focal point. Here’s the math behind potential gas price spikes.

KEY TAKEAWAYS

-

US strikes on Iranian military and strategic targets escalated tensions beyond last year’s limited operation. Retaliation is already underway, increasing the probability of prolonged regional instability.

-

Oil markets reacted immediately, with Brent and WTI surging at the open before partially retracing. The move reflects both fresh risk and an existing buildup of geopolitical premium.

-

The Strait of Hormuz carries roughly 20 million barrels per day, about one-fifth of global consumption. Even partial disruption for four weeks could delay 280 million barrels of supply.

-

A sustained $10-$20 rise in crude could translate into 25-50 cents per gallon at the wholesale gasoline level. Regional constraints could push that impact to 30-60 cents at the pump.

-

The most lasting market impact is likely higher energy prices feeding into inflation expectations. That dynamic pressures the Fed’s path and weighs particularly on rate-sensitive growth stocks.

MY HOT TAKES

-

The immediate equity selloff is not the core risk; the inflation impulse is. Energy shocks change monetary policy narratives faster than headlines do.

-

Markets were already pricing rising geopolitical probabilities before the first missile flew. This is an acceleration of trend, not a clean break from calm.

-

A formal closure of Hormuz is not required to disrupt supply. Insurance withdrawal and risk aversion can effectively shut the strait without a decree.

-

Gasoline prices have disproportionate psychological and political weight. A visible rise at the pump can shift consumer expectations quickly.

-

Geopolitical confrontations rarely produce clean winners. Energy markets, inflation, and valuations often leave both sides economically scraped up.

-

You can quote me: “Gasoline prices are psychologically powerful–they are the inflation number that consumers see every single day.”

Say uncle. Sorry to start off the morning with a graphic example of violence, but… well, these times kind of allow us to relax the standards. I remember horseplaying with my friends as a kid. It was mostly orderly, but occasionally, tensions flared. One of those flares found me holding down a friend after a wrestling bout gone wrong–it was for real. Once I had him pinned, my first thought was that I had won. Almost immediately after that thought, I was overtaken by fear. What would I do next? I couldn’t hold him down forever. I am not sure if it is just an American thing in the 1960s, but saying the word “uncle” was the codeword for friendly submission. However, in this case it WAS real. If I let my friend loose, he was likely to immediately retaliate after I humiliated him. I was effectively just as stuck as my opponent.

I realized at a young age right then and there that all actions have consequences.

Over the weekend, those consequences became very real in the Middle East. What began as rising probabilities and positioning last week turned into coordinated US strikes on Iranian military and strategic targets. This was not a pinprick operation. It was broader in scope and more forceful than last year’s Operation Midnight Hammer. The targets were meaningful. The messaging was deliberate. And the response risk is real. Not unexpectedly, Iranian officials have vowed retaliation, and that retaliation is playing out in real time as the country has launched a massive barrage of missile and drone strikes across the region.

Now let's talk about what matters most to your portfolio this morning. Brent crude spiked as high as 13% to above $82 a barrel at the open before paring back to around $79, while WTI rose more than 8% to cross $72 per barrel. Oil had already been building a risk premium all week–it was above $70 before the first missile flew–so what you are seeing this morning is a continuation and acceleration of a move that was already underway, not a clean break from calm. Equities, as I predicted in the February 19th post (check it out here: https://blog.siebert.com/wargames-war-risk-and-wall-street ), are leading with the vulnerable names: Dow futures fell 350 points at the open of futures, and the rate-sensitive, high-growth corner of the market is taking the first and hardest punch, exactly as I flagged. Gold is up sharply, rising 2.3% to $5,367 per ounce, and Treasury yields are hovering right around 3.97%, actually higher by a few basis points. The gains in yields may already be reflecting the market’s assessment of inflation impacts. Additionally, there is a noticeable bid in usual-suspect defense stocks. The XLE/ITA/GLD framework I laid out on February 19th is working. The question now is how long you hold it–and that answer depends almost entirely on one 21-mile-wide waterway.

The Strait of Hormuz is the jugular of the global energy system, and right now, it is bleeding. Let me give you the actual anatomy of why this matters so much. Roughly one-fifth of global oil consumption moves through that narrow channel each day. On average, about 20 million barrels per day of crude and petroleum products transit that waterway. In addition, a significant portion of global liquefied natural gas exports–particularly from Qatar–flow through the same strait. It is not just about oil. It is about global energy plumbing. Even a partial disruption, or simply a slowdown due to risk premiums and insurance surcharges, can tighten supply expectations very quickly. Iran has stated it is not formally closing the strait–but that statement is functionally irrelevant. The Strait of Hormuz is effectively closed for commercial shipping despite technically remaining open. Insurance withdrawal is doing the work that a physical blockade has not–the outcome for cargo flow is largely the same. Maersk has suspended all vessel crossings until further notice, tanker owners and oil majors have pulled back, and hundreds of tankers are sitting stationary on either side of the strait, waiting. The war zone does the closing. You don't need a formal decree.

Now, let’s do the math that no one wants to do. Global oil demand runs around 100 million barrels per day. If 20 million barrels per day normally pass through Hormuz and even half of that flow is effectively delayed or rerouted for four weeks, that is a temporary disruption of roughly 10 million barrels per day. Over 28 days, that equates to 280 million barrels of delayed supply. Strategic reserves and alternative routing can offset some of this, but not all of it instantly. In tight markets, it does not take a full 10% global supply shock to move prices. A perceived shortfall of even 2 to 3 million barrels per day sustained for several weeks can push crude meaningfully higher because pricing reflects marginal supply.

Now translate that to the gas pump. One barrel of crude yields about 42 gallons of refined products, and roughly half of that becomes gasoline. So, call it 20 gallons of gasoline per barrel for simplicity. If crude rises $10 per barrel and refiners pass through most of that cost, that is roughly 25 cents per gallon at the wholesale level. A $20 move? Now you are talking about 50 cents per gallon. Add in regional refining constraints and distribution markups and the range could easily be 30 to 60 cents higher at the pump over a matter of weeks if crude sustains those gains. Even if the Strait is not officially closed, a four-week effective disruption that lifts crude into the $90 to $100 range could very realistically translate into a noticeable jump in gasoline prices nationwide.

And remember, gasoline prices are psychologically powerful. They are the inflation number that consumers see every single day. We were just starting to have a serious conversation about whether inflation was sticky or merely stubborn. A sustained energy shock changes that narrative. At best, it gives the Fed an excuse to keep policy restrictive for longer. At worst, it actually re-accelerates headline inflation and seeps into expectations. Energy feeds transportation costs. Transportation feeds goods prices. And suddenly, what looked like a steady glide path lower becomes another plateau.

This is the most likely lasting negative impact on markets. Not the missiles themselves. Not even the initial equity selloff. It is the secondary effect of higher energy prices colliding with an already cautious Federal Reserve. Growth stocks feel that first because their valuations are most sensitive to discount rates. But over time, elevated energy costs tax consumers and corporate margins alike. The backyard brawl becomes less about who threw the first punch and more about who can afford to stay in the ring.

Which takes me back to that wrestling match. In the moment, I thought I had won. I had my friend pinned. But the reality was more complicated. I couldn’t hold him down forever. If I let him up, he might swing. If I didn’t, I was stuck. Now that I think about it, I honestly can’t remember whether it was me who “won” that match or whether it was him. What I do remember is that we were both scraped up and breathing hard by the end of it. We effectively both lost. We are, thankfully, still friends today.

Geopolitics is rarely a clean victory. Energy markets do not care about pride. Inflation does not care about narratives. Actions have consequences. This week, investors need to think less about the first punch and more about what happens after someone says uncle–and whether anyone actually does.

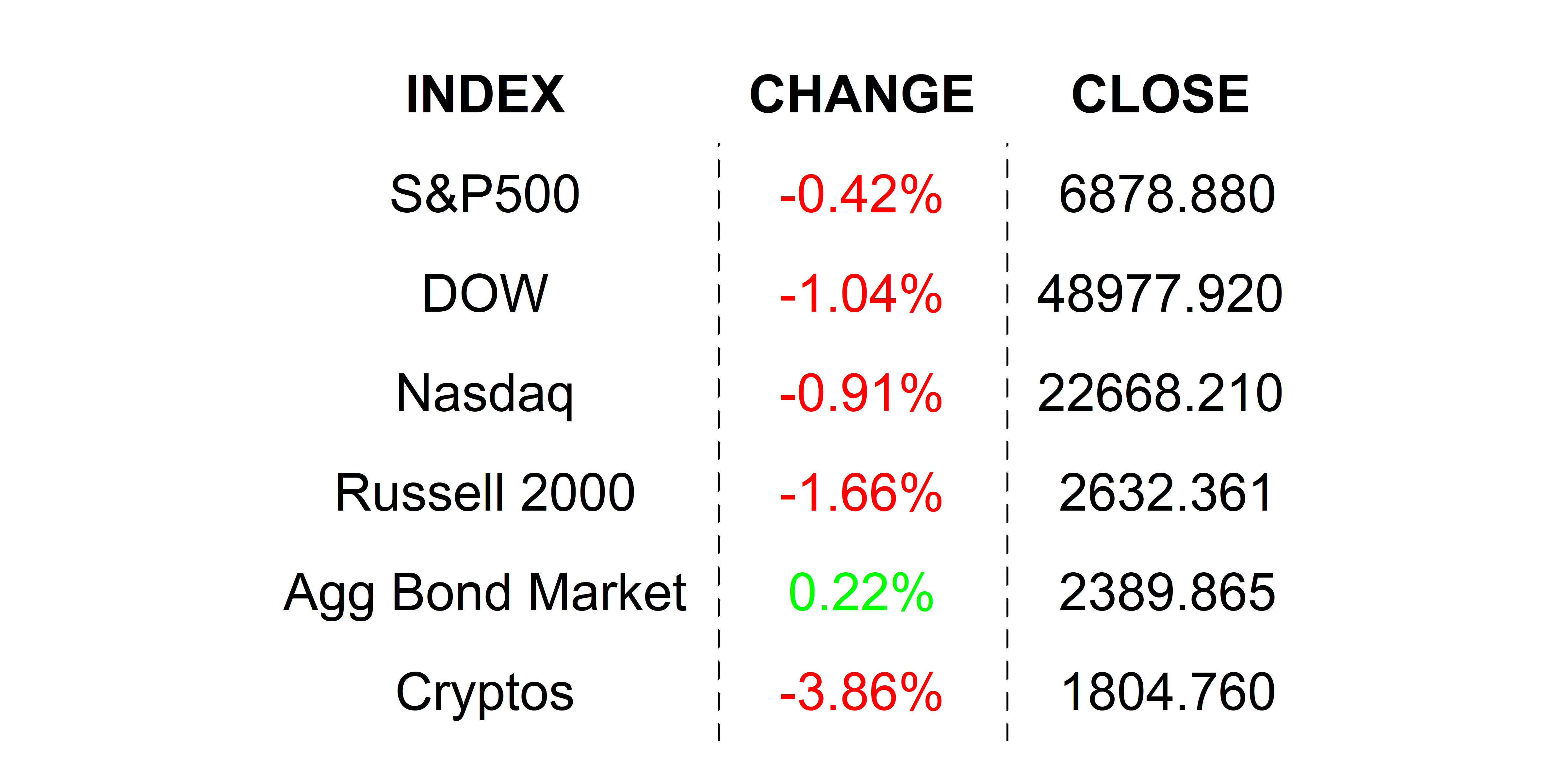

FRIDAY’S MARKETS

Stocks continued their slip on Friday as the SaaS-pocalypse continued to pressure software and broader-tech stocks. Financial stocks caught some pressure on Friday on continued fears of a brewing problem in private credit with fraud reports about a large private-credit funded direct lender in the UK. The last trading day of the month closed with investor nerves raw and exposed.

NEXT UP

-

ISM Manufacturing (February) may have slipped to 51.5 from 52.6.

-

Later this week: more important earnings in addition to ADP Employment Change, more PMIs, Fed Beige Book, Retail Sales, and monthly employment figures. Download the attached economics and earnings calendars to gain the high ground.

-

Important earnings today: Sealed Air Corp, Venture Global, Firefly Aerospace, Riot Platforms, Norwegian Cruise Lines, MongoDB, PlugPower, and AES Corp.