.png)

Markets rallied hard on a fragile ceasefire, but the underlying risks have not been resolved. The path higher may be real, but it is still full of sharp turns.

KEY TAKEAWAYS

-

The recent rebound in stocks was driven by relief, not by a true change in the underlying fundamentals. The major geopolitical, inflation, and policy risks remain unresolved.

-

A two-week ceasefire is not the same thing as a durable peace agreement. Markets reacted as though a lasting solution had arrived when the evidence suggests otherwise.

-

The Strait of Hormuz remains a central risk to global energy markets and inflation. Oil may have fallen sharply in one session, but prices remain far above pre-conflict levels.

-

The Fed is still stuck in an uncomfortable position with no easy policy move. Higher energy prices and sticky inflation make rate cuts harder to justify, even as growth slows.

-

The long-term case for equities remains intact, especially where earnings growth is still strong. The danger is not owning stocks, but reacting emotionally to every headline along the way.

MY HOT TAKES

-

The market celebrated a pause and treated it like a peace treaty. That is a very generous interpretation of a very temporary development.

-

Both the panic selloff and the explosive rebound were exaggerated. The market has now managed to price in disaster and perfection in the span of a few weeks.

-

Headline-driven investing is turning the tape into a casino. That kind of environment punishes conviction that is not backed by actual work.

-

The Fed’s situation is getting worse, not easier. Energy inflation and geopolitical risk just added another layer of paralysis to an already messy policy setup.

-

The path to new highs is real, but the smooth ride fantasy is not. Investors are going to have to earn their way through this tape with discipline and patience.

-

You can quote me: “Both the worst case and the best case have now been priced in, and the best case hasn't happened yet.”

Sharp turns ahead. How would you like it if I told you that the stock market is going to be just fine? You would love it, of course, but you may not believe me–you would want to see it with your own eyes. I get it. We have so much data at our finger tips these days, and it’s updated by the minute or even second. In this day and age, we have trained ourselves to expect timely information. We expect it, so much so that sometimes, we generate conclusions on the fly before we even qualify the information.

A news headline here, a Tweet there, an eavesdrop of a person–a complete random stranger–trading their brokerage account next to you on the train–she may even notice and tell you what she’s buying and why–after all, sharing is THE thing these days. That's a lot of information–data. But not all data is tradable data, though it may seem like it is. My longtime regulars have heard me say many times that the market rarely does what is convenient for you at any given time. You may be desperate for a turn of luck–convinced that your thesis is right–logic on your side. A move would be convenient–even destined–but maybe not just yet. That reality occasionally puts investors in a vulnerable position, leading them to misread data and take it at face value. The usual result: pain.

The past several months has been challenging for investors used to having everything go their way–well not everything, but enough to cause them to forget the mistakes, leaving them destined to make those mistakes again and again–and again. These past few months saw their long-winning tech trades veer off the track and get overtaken by companies in sectors that have nowhere near the growth potential and earnings strength of tech. It has been dubbed a "rotation" to quality, whatever that means. But it worked.

For folks on the hunt for growth AND value, which are two things that rarely co-exist, the rotation has provided some opportunities. When would the rotation reverse? Add a waffling Fed with an outgoing leader intent on fighting inflation and satisfied with tepid job numbers, and the equation gets even more challenging. Tech, after all, needs falling interest rates to rally. Does it really? Well it helps “on paper” but not really. Growth stocks need continued and solid earnings growth to remain viable. Ok, I am veering now, but I want to capture the confusion faced by investors.

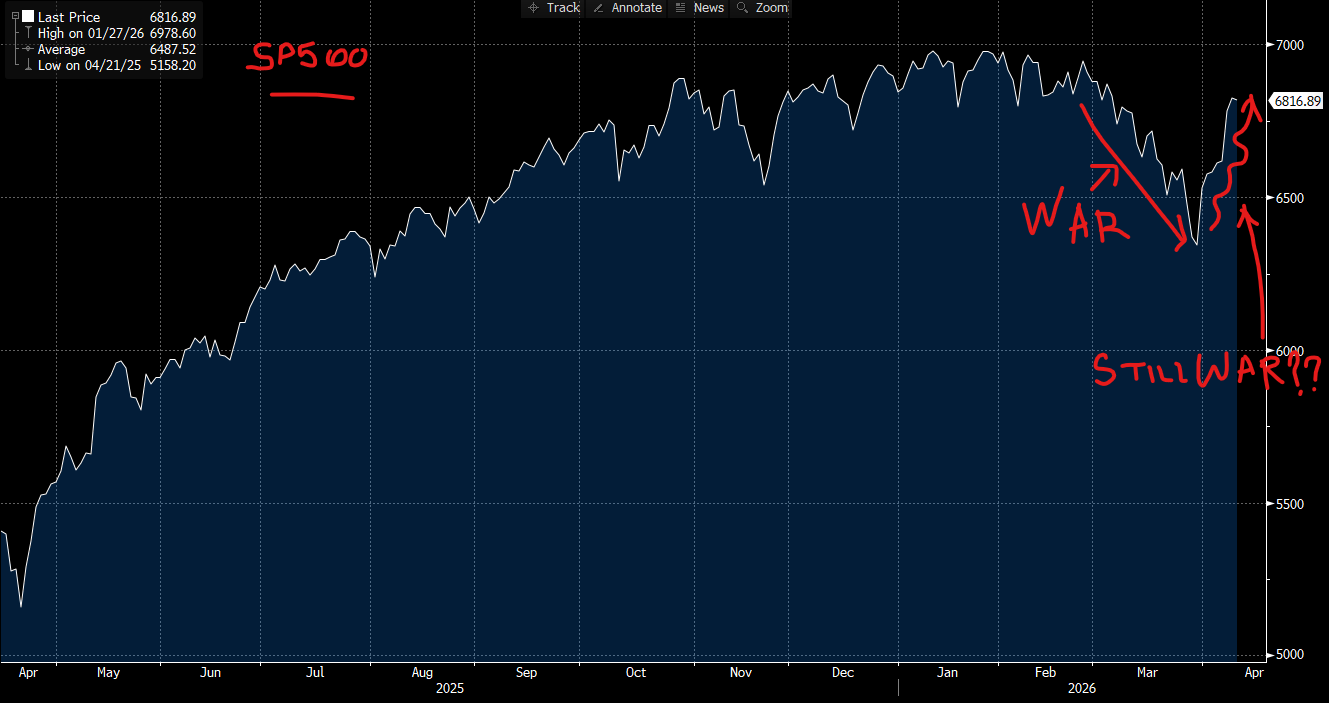

Now add to this mix some even bigger challenges with the Iran conflict erupting a few weeks back. Markets were treated to their worst-case scenario playing out. A conflict that did not just last a single day, but several weeks with an indeterminate end. Making matters worse was another worst-case scenario–not quite expected by most investors–the shutting down of the Strait of Hormuz, blocking 20% of the world’s crude and LNG supply. Markets, rightly so, reacted negatively to what would surely further inflame an already unforgettable inflation scenario. And then it would all change with a series of social media posts and soundbites. Check out the following chart and keep reading.

This is a chart of the S&P 500 over the past year. You can see the rocket ride from last April’s lows through the end of the year. A bit of lost momentum at the start of the year and then the rapid decline resulting from the onset of the Iran conflict. When I look at this chart, the first question that comes to my mind is how did we go from that sizable decline and drawdown to that huge boost which included seven consecutive positive closes (two large ones). That leaves us near enough to the indexes all-time high to consider it a target again. Is the war over? Is the Strait of Hormuz open? Has the Fed indicated that it would resume rate cuts soon? No, no, and no.

The answer to all three of those questions being no is, in my view, the most important information to focus on this Monday morning. What you just witnessed in the market over the past week was not a fundamental shift in the underlying conditions. It was a relief rally, and relief rallies, by their very nature, are not built on solved problems. They are built on the temporary absence of fear.

Let me be precise about what actually happened. The US and Iran agreed to a two-week ceasefire. Two weeks! Not a peace treaty. Not a diplomatic resolution of Iran's nuclear ambitions, its regional posture, or the sanctions framework that has defined the relationship between Washington and Tehran for decades. A two-week pause. And within hours of the announcement, the speaker of Iran's parliament declared on social media that the ceasefire had already been violated. Hours. That detail did not make the banner headlines, but it should have, because it tells you everything you need to know about the durability of what markets just celebrated.

The Strait of Hormuz, through which roughly 20% of the world's oil supply normally flows, has not been declared fully open by any independent authority. Here is the number that caught my eye when I saw it: on the day the ceasefire was announced–the very day markets exploded higher–only four ships passed through the Strait. Four. That was the lowest transit count of the entire week. Eleven ships had passed through the day before. 😯 The infrastructure for a genuine reopening does not yet exist, and maritime insurers, who must underwrite the cargo on those tankers before captains will risk the passage, remain deeply cautious. Goldman Sachs has been direct about the math: if the Strait remains constrained for even one additional month, Brent crude could average above $100 a barrel for the remainder of 2026. And here is what the rally seemed to miss–even after oil's historic single-day plunge on ceasefire day, both WTI and Brent remain more than 40% above where they traded before the conflict began. The structural damage to refining infrastructure does not heal overnight, and Exxon Mobil disclosed that the war cost it roughly 6% of its total global output. 6% from one of the largest energy companies on earth. That is not a rounding error. None of this changed because of a social media post.

What the market did, in essence, was price in a best case that has not yet actually occurred. Think carefully about what that means for you as an investor. A few months ago, the market priced in a worst case–the conflict, the Hormuz closure, the inflation resurgence, the Fed trapped between a rock and a hard place with no clean move available. The index sold off hard and fast, as you can see in that chart. Then, with a ceasefire announcement that carries a two-week expiration date and competing claims about whether it is even holding, the market sprinted back toward its all-time high. Both the worst case and the best case have now been priced in, and the best case hasn't happened yet. That is the trap.

To be clear, this is not me telling you to sell stocks. That would be the wrong conclusion, and frankly it would be the same mistake in the opposite direction–reacting to the data in front of you at face value rather than qualifying it. The investor who sold in a panic when the conflict broke out made a painful error. The investor who chases this rally with full conviction that the worst is behind us may be setting themself up for a different kind of pain. The worst decision in this environment, and I want to be very direct about this, is to keep reacting to every headline. Good news, bad news, a Trump post, an Iranian parliament statement, a Fed governor walking to a microphone–all of it has been moving markets by multiple percentage points in both directions. That is not an investing environment. That is a slot machine.

What I want you to understand is that the Fed's position has not improved. If anything, the Iran situation has added a new and deeply uncomfortable variable to an already impossible equation. Jerome Powell mentioned tariffs twenty-four times at his March press conference. He was unambiguous that inflation remains elevated in part because of policy decisions that are outside the Fed's control. Now layer on top of that an energy price shock that, even with a ceasefire, has not fully unwound. Reminder: oil is still 40% above pre-war levels as I write this. The Fed cannot cut rates into rising energy prices and sticky goods inflation without risking a serious credibility problem. It cannot hold indefinitely without the economy slowing further. It cannot raise rates without triggering exactly the kind of credit stress in private markets and corporate debt that has been quietly building all year. There is no clean move. That paralysis does not resolve because of a two-week truce that one party declared broken before the ink was even dry.

So what do you do with all of this? You view the signals carefully, and you resist the very human urge to treat each new signal as the final word. The ceasefire may hold. The negotiations in Islamabad may make progress–though the latest news implies that it is not getting there anytime soon. The Strait of Hormuz may gradually reopen, maritime insurance may normalize, and oil prices may drift back toward pre-conflict levels over the coming months. The Fed, freed from the worst of the energy inflation overhang, may then find the room to resume its rate-cutting path. Corporate earnings, which have proven more resilient than most expected, may hold up well enough to justify current valuations. All of that is possible. Some of it is even probable over a reasonable time horizon.

But between here and there, expect more flip-flops. Expect more whipsaws. Expect the market to price in outcomes that haven't happened yet, and then reprice sharply when reality arrives with an asterisk attached. The two-week clock on this ceasefire is already ticking, and when that deadline approaches you will very likely see the kind of volatility we have already lived through play out again in some form. The pattern is now well established. A threat, a deadline, a social media post, a market lurch in one direction, followed by a complication, followed by a lurch in the other. Position yourself accordingly. Not with panic, and not with euphoria, but with clear eyes.

Here is what I am confident telling you: stocks are going to be just fine. I mean that sincerely, and I am not saying it to make you feel better. The underlying earnings power of many of the recent winners has not been destroyed by a month of conflict or a year of tariff noise. The economy, while slowing, has not collapsed. Consumers are still spending, selectively but meaningfully. Technology, for all the rotation drama, retains earnings growth that most of the sectors that temporarily outperformed it can only dream about. The road back to and through the all-time high is a real road, not a fantasy. But it is a bumpy road, and the biggest mistake you can make right now is to assume the bumps are behind you simply because last week felt smooth. The market has shown you both ends of the range. The worst case was priced in. The best case has been priced in ahead of schedule. Now comes the hard work of reality filling in the middle.

FRIDAY’S MARKETS

Stocks closed out their best week since November on Friday, with the S&P 500 ending essentially flat on the day, down by -0.11%, the Nasdaq edging up 0.35%, and the Dow slipping by -0.56% as a hotter-than-expected CPI reading and an all-time low University of Michigan consumer sentiment print took the edge off the ceasefire euphoria. For the week, the S&P 500 gained roughly 3.6%, the Nasdaq surged nearly 4.7%, and the Dow added about 3%.

NEXT UP

-

Existing Home Sales (March) may have slipped by -0.8% after climbing by 1.7% in the prior month.

-

Later this week: earnings season begins along with PPI / Producer Price Index, NFIB Small Business Optimism, more housing numbers, The Fed Beige Book, and Industrial Production. Check back each day–you don’t want to be the last one to find out what’s up.

-

Fed Governor Stephan Miran is speaking today.

-

Important earnings today: Goldman Sachs and Fastenal.