.png)

Crude, CPI, Fed policy, and tech valuations—this is how one geopolitical shock ripples through markets.

KEY TAKEAWAYS

-

Oil is a finite commodity governed by supply and demand, and geopolitical conflict can disrupt production or transit routes, particularly through the Strait of Hormuz. When nearly 20% of global oil flows through a narrow shipping lane, duration of disruption becomes the critical variable.

-

A 15% rise in crude, from $80 to $92, can translate into a meaningful increase in gasoline prices and directly add roughly 0.25 to 0.30 percentage points to headline CPI. Second-order effects through transportation and embedded petroleum inputs can lift that contribution closer to 0.40 to 0.50 percentage points.

-

Higher inflation expectations can quickly alter the Fed’s reaction function. A contemplated easing cycle from 3.75% to 3.25% can evaporate if inflation drifts back toward 2.5% or 2.6%.

-

Growth stock valuations are highly sensitive to discount rates. A 50 basis point shift in expected policy can move terminal multiples by more than 10%, even without any operational change in the company.

-

Markets often reprice rate expectations faster than physical supply disruptions resolve. Oil may normalize with time, but valuation compression can occur within days.

MY HOT TAKES

-

Geopolitical shocks matter less for drama and more for duration. The longer supply routes remain impaired, the greater the structural inflation risk.

-

Oil price spikes are not just energy stories; they are macro transmission mechanisms that ripple through inflation, Fed policy, and equity valuations. The real story is the discount rate, not the headline.

-

Markets frequently overshoot when repricing rate expectations. A “no cut” narrative can be fully priced in long before the physical oil shock proves temporary.

-

Growth companies with intact secular demand can recover quickly once rate fears subside. The valuation hit is often mechanical rather than fundamental.

-

Investors should avoid simplistic narratives like “AI jitters.” Serious investing requires understanding the mathematical linkage between crude, CPI, the Fed, and discounted cash flow models.

-

You can quote me: “Oil doesn’t just fuel cars–it fuels valuation models.”

Degrees of separation. My puppy Eloise is really smart and represents generations upon generations of selective genetic breeding enabling her to read my facial expressions and manipulate me to get exactly what she wants at any given time. That said, she is pretty easily manipulated as well–with a simple biscuit. This is a well-understood causal relationship.

Similarly, when you attack a desperate regime that has stockpiled munitions for decades, that has a dominant strategic position in a key commercial shipping lane, that sits within striking range of the largest crude and LNG producers, and that itself possesses the third largest proven reserve of crude oil in the world, one would expect markets to react.

How much the markets react, of course, would be determined by just how much and for how long a conflict would jeopardize the production or energy products. Let’s start with the basics. My long-time followers know one of my favorite quotes: “oil IS the oil of all industry.” It is the lubricant of all commerce showing up in places that you least expect. Yes, it’s in plastic, in your cosmetics, on the road in front of your home, and even finds its way into those favorite stretchy pants of yours. Oh yeah, it makes your car run, airplanes fly, ships sail, and your lights turn on. It would not be difficult to trace a portion of the cost of almost everything you use on a daily basis to crude oil. That said, when it goes up in price, so does the cost of all those things at one level or another.

Crude oil is a finite commodity and its price, is therefore, well understood to be governed by one of the most elemental microeconomic tenets: supply and demand. That sensitivity is, in fact, exploited daily by the world’s largest oil producers to manipulate the price of oil. Cut supply, prices go up, throttle up production and prices go down. It’s that basic.

Supply control is typically manipulated by literally controlling the rate at which the stuff is pulled out of the ground, and further upstream by controlling the pace at which it is refined to usable distillates. Got it? It is that easy to manipulate the prices of… em, everything. Those stretchy pants, the oil that lubricates the forklift that puts it on a truck, that fuels the truck that delivers it to your local retailer, the fertilizer that helps grow the grain in the bread in the sandwich that fuels that not-so-friendly sales person that helps you buy those pants, and the petroleum that runs your overpriced Uber ride home from the store.

There is more than one way to cut crude production and raise the price of oil–and ultimately, everything–if you have been following my logic.

You can literally blow up oil production facilities or choke off the 21-mile-wide Strait of Hormuz through which nearly 20% of the world's oil transits daily. Yep that would do it. It is, in fact, that simple to degrade global commerce. Several weeks ago, I gave you the playbook for three Iran attack scenarios. At the core of each scenario was oil and the level and duration an attack might have on its price. The lowest-impact scenario had results similar to Operation Midnight Hammer from Back in June of 2025 when the US bombed Iran’s nuclear facilities in a one-and-done military action with no impact on crude production. Stocks would dip while crude and gold would jump–all temporarily in an emotional response. A longer conflict–perhaps weeks–would see a similar response but with more intensity and a slower reversion back to mean. An undefined-length conflict topped the risk list and included the closing down of the Strait of Hormuz for an extended period of time. This would, as one would expect, cause crude to spike meaningfully. Though it is not completely clear yet–nothing ever is in war–it appears that we have quite quickly worked through scenario 1 and scenario 2, and that we are on the brink of scenario 3.

With the Strait of Hormuz shut down, LNG production halted in Qatar, energy facilities being bombed in the region, you should not be surprised that WTI crude this morning is some 14% higher than it was at last Friday’s close where an attack seemed likely, but had not yet occurred. You would, therefore, not be surprised to see energy companies, which benefit from higher crude prices, on the rise. But let’s take it a step further this morning. Why would all of your favorite tech stocks fall in response to the rise in crude oil prices? Please, please don’t say “AI jitters or Saas-pocalypse!”

Ok, strap on your seatbelt, we are going to do some grownup math here. Sorry, but if you are serious about investing in stocks, you need to understand this–it’s for your own good. Assume crude rises 15%. If we were at $80 per barrel, that takes us to $92. Historically, a $10 move in crude translates into roughly 20 to 25 cents per gallon at the pump (see my analysis in yesterday’s note: https://blog.siebert.com/hormuz-the-21-mile-inflation-machine). A $12 move would therefore imply something closer to 25 to 30 cents. Gasoline carries a weight of roughly 3% in CPI. Energy more broadly is closer to 7%. If gasoline prices rise 8% to 10% as a result of that crude move, you are talking about a direct contribution to headline CPI of approximately 0.25 to 0.30 percentage points on an annualized basis. That is before second-order effects.

Now layer in transportation services, airfares, shipping costs, and goods that embed petroleum inputs. Even if pass-through is partial, say another 0.10 to 0.20 percentage points over several months, you are quickly staring at a potential 0.40 to 0.50 percentage point bump to headline CPI! Core PCE, which is the Fed’s favorite inflation gauge, will move less, because it strips out food and energy, but it is not immune. Higher diesel raises goods transportation costs. Airlines can hedge, but not forever. Chemical inputs matter. A conservative estimate might add 0.15 to 0.25 percentage points to core PCE over time.

If the Fed was contemplating cutting rates from 3.75% to 3.25% over the next several meetings, and suddenly the inflation path shifts up by even 0.30%, the reaction function changes. Remember, the Fed targets 2%. If core PCE drifts from 2.2% back toward 2.5% or 2.6%, that is no longer “mission accomplished.” That is “hold your horses.” A 50 basis point easing cycle from 3.75% down to 3.25% can evaporate quickly in the face of renewed inflation pressure,, especially based on recent hawkish rhetoric by an increasing number of FOMC members. Higher for longer becomes not a threat, but a necessity.

Now let’s bring this into valuation land, because this is where it hits your wealth. Take a high-growth company like NVIDIA. The market is not valuing it on next quarter’s earnings. It is valuing it on a stream of cash flows ten years out. In a simplified discounted cash flow framework, the value of a stock equals the present value of future cash flows discounted by a rate that includes the risk-free rate plus a risk premium.

Assume NVIDIA is expected to generate $10 per share in free cash flow five years from now, growing at 20% annually for several years thereafter. If the appropriate discount rate is 8.75%, reflecting a 3.75% Fed Funds rate plus a 5% equity risk premium, the present value of that $10 received in five years is $10 divided by 1.0875 to the fifth power (stay with me 🤓), which is about $6.58. Now decrease that discount rate by 50 basis points to 8.25%, consistent with a Fed cut to 3.25%. The present value becomes $10 divided by 1.0825 to the fifth power, which is about $6.73. That may not sound dramatic on one cash flow, but now apply that 50 basis point difference across an entire decade of rapidly growing cash flows and a large terminal value.

The terminal value is where the real sensitivity lies. Terminal value is the total value of all future cash flows, forever, ‘till the end of time, at some future point. If you assume a long-term growth rate of 4% (that means you expect the company to grow earnings at that pace forever) and a discount rate of 8.75%, the capitalization multiple on terminal cash flow is roughly 1 divided by (0.0875 minus 0.04), or about 21.1 times. Lower the discount rate to 8.25%, and that multiple rises to 1 divided by (0.0825 minus 0.04), or roughly 23.5 times. That is more than a 10% increase in the terminal multiple from a mere 50 basis point shift in expected Fed policy. For a stock whose value is heavily weighted toward terminal expectations, that is not trivial. That is double-digit percentage upside or downside in theoretical value without any change to the company’s operations whatsoever. I am hoping that even if you didn’t exactly follow the math, that you understand the mathematically causal relationship between Fed policy and stock valutions–especially your favorite growth stocks.

So yes, crude affects more than the synthetic fabric in your stretchy pants. It can ripple through inflation expectations, alter the Fed’s path from 3.75% to 3.25%, lift or lower the discount rate, compress or expand valuation multiples, and take a bite out of your portfolio even if Jensen continues to sell every GPU he can fabricate.

But here is the important nuance. The price of crude is real. Whether speculative or not, it trades at a real clearing price. If tankers cannot pass through a shipping lane, the marginal barrel becomes more expensive. Some costs cannot be avoided. Airlines will pay more. Trucking companies will pay more. Consumers will feel it.

Theoretical stock values, on the other hand, are discounting machines. They are speculating not just on today’s 3.75% Fed Funds rate, but on whether it will be 3.25%, 3.00%, or something else entirely three, five, even ten years from now. That is where markets can overshoot. A 50 basis point “no cut” narrative can be priced in within days, even if the physical oil shock ultimately proves temporary.

Crude will normalize when supply routes reopen and production resumes. It may take weeks or months for inventories to rebuild and confidence to return. But growth companies with intact demand curves and secular tailwinds can recover far more quickly once rate fears subside. We have seen that movie before.

So should you panic? No. Should you be vigilant? Absolutely. There will be dip-buying opportunities. There always are. But risk must be gauged appropriately. Time is still very much an unknown variable in any conflict. Duration matters more than drama.

And that brings me back to my Eloise. I think I am manipulating her with a biscuit. She sits. She waits. She obeys. But somehow, she always ends up with the treat. Markets are similar. We think we are rationally allocating capital based on neat causal chains. In reality, we are often reacting to incentives placed in front of us. Oil spikes, we sell tech. Tech dips, we buy the biscuit.

Just make sure you know who is manipulating whom.

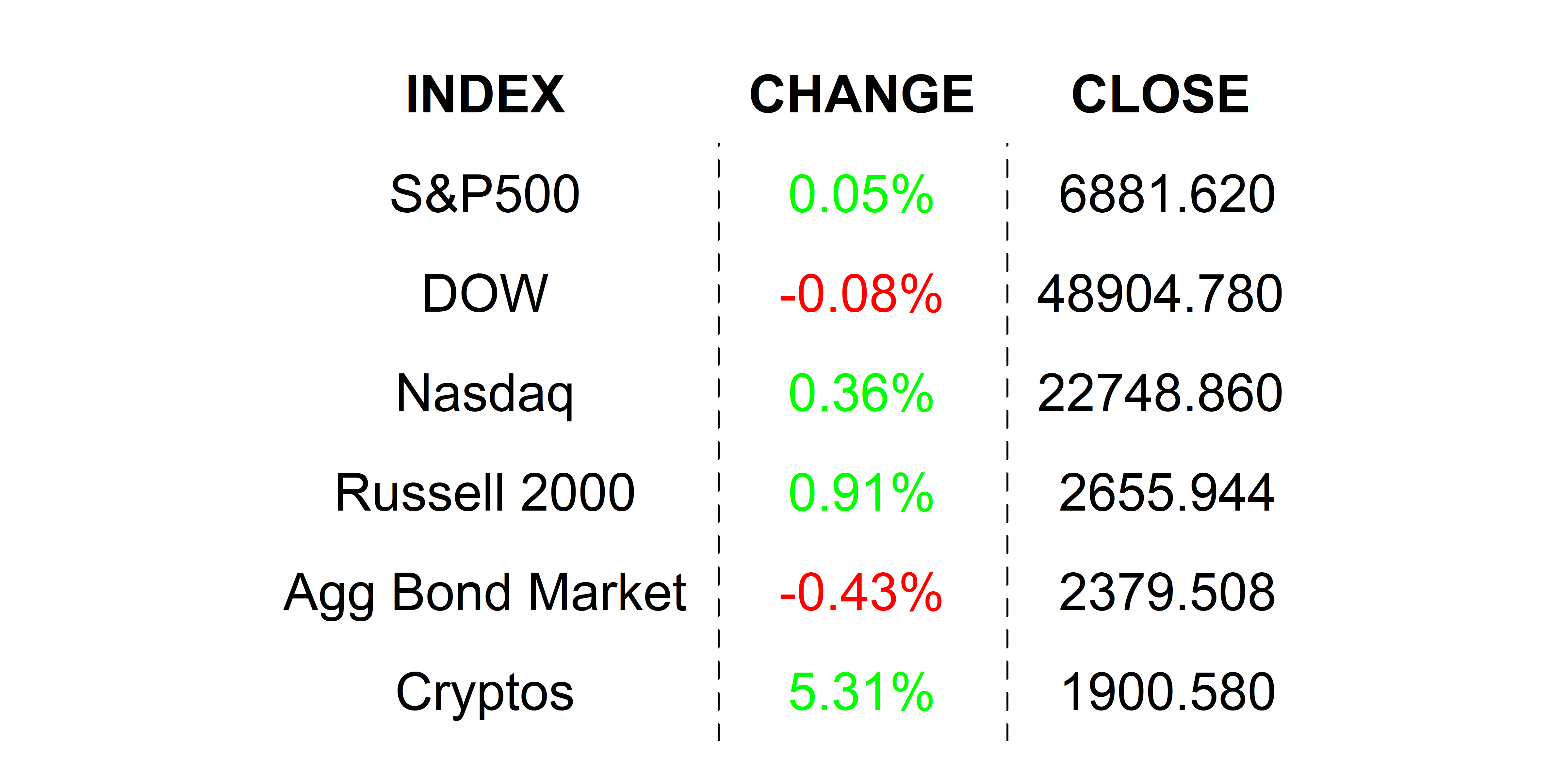

YESTERDAY’S MARKETS

Stocks took a wild ride yesterday, starting the session deeply in the red in response to the start of the Iran conflict. Dip buyers rushed in to buy already-beaten-down tech shares resulting in a mixed close well above session lows. Treasury yields rose reflecting inflation fears and crude spiked.

NEXT UP

-

No major economics numbers today, but we will hear from the Fed’s Willaims and Kashkari where they are likely to comment on inflation worries related to rising energy prices.

-

Important earnings today: Versant Media, Best Buy, AutoZone, Target, Ross Stores, Crowdstrike, Gitlab, and Rayonier.