Breaking down the Hormuz threat and what investors should expect next.

KEY TAKEAWAYS

-

Mined games title is intentional--a wordplay on the strait of Hormuz

-

The U.S. bombed Iranian nuclear sites--likely timed with carrier group deployment–but it was a clever ruse

-

Markets had already priced in strike risk--focus shifts to Iranian retaliation

-

The Strait of Hormuz remains the main geopolitical and market risk

-

Escalation to “severe” threat is possible but not probable

MY HOT TAKES

-

Markets hate unknown--Saturday’s strike removed that element

-

Hormuz is the real risk--but Iran can’t sustain a full closure

-

Investors should focus on long-run trends--not headline volatility

-

The press and public may overreact--but the market won’t if it’s priced in

-

This is a textbook case of how known risks become absorbable events

-

You can quote me: “Escalation to a severe threat is possible—but not probable. And markets already know the difference.”

Mined games. Did you pick up on that, or did you feel like I made a typo? Read it again. Ok, now we are ready to get into it. I am sure that you, like me, have been riveted to the news this past weekend since we first learned that the US bombed some of Iran’s nuclear sites on Saturday night (NYC time). I was out with my family celebrating my birthday when my son thrust his smartphone in my face showing me a retweet from the President. At that moment–and I kid you not–every single person at the table jumped on their phones to confirm that the tweet was authentic. Within minutes, I got my first phone call from the press for comment. It was expected–I flashed my phone to my wife, and headed to a quiet corner of the restaurant to take the call. Stay tuned for what I said.

All weekend, I was monitoring open source intelligence and just about any source I could find to get a clue of what might happen. After the President announced on Friday that he would put off a decision to strike at Iran’s nuclear capability for two weeks to allow diplomacy–which we now know was a clever ruse–I was convinced that the strike was inevitable and most likely a logistical allowance as two additional carrier strike groups steamed to the theater. The thesis that I shared with the press was that these next two weeks would be filled with tension and market volatility that would only be resolved if and when a strike occurred or Iran stood down.

I wouldn’t dare share that my likely case scenario was indeed a strike at some point. I know that many of my colleagues also shared a similar opinion, that it was not if but when. We also knew that a new risk would emerge if the US struck. All-out regional war was certainly a worse-case scenario, but unlikely given that the other regional powers view Iran as a source of instability. Knowing that the regime has already been backed into a corner, it would likely not simply back down. No. Some sort of tense conflict appeared inevitable. The only questions were how big and how long would they last.

Ten days ago on a sleepy Friday, Wall Street awoke to news that Israel had struck Iranian nuclear facilities taking markets by surprise. While the possibility existed, it was not considered likely at the time, so it was, indeed, what we call in stats a tail event. That is when something that is highly unlikely to happen… happens.

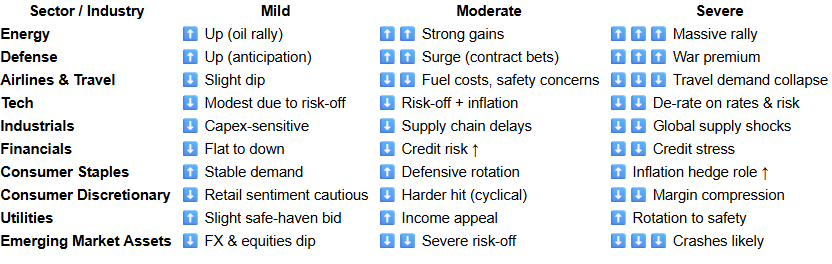

Markets reacted accordingly. Crude oil gained and stocks dipped but closed off their lows. I penned a rather lengthy newsletter/blog post on that day detailing all the risks associated with the attack along with the various scenarios. Read it here. If you missed it, I will tell you that I highlighted the Strait of Hormuz closure as being the biggest risk. I created a threat matrix that showed what results would be in a mild, moderate, or severe conflict. At that point, I thought the conflict was at a mild threat level.

In the days that followed, it became clear that Israel was dominating Iran militarily, only targeting strategic targets. Israel soon controlled Iranian airspace. As it became clear that Israel had clear strategic goals, Iranian nuclear capability, a severe conflict became less likely, though the Strait of Hormuz remained one of the single biggest weak points in the hypothesis.

Why am I going through all of this history this morning? Well, I want you to realize that I am not the only strategist contemplating these potential outcomes. In other words, the market has already factored in much of what we have woken up to this morning.

The US indeed bombed Iranian nuclear facilities and has made it clear that it is not seeking a larger conflict. The Sunday press circuit and political opponents tried to agitate and troll administration officials into talking about “regime change,” but thankfully, they have been unsuccessful (except maybe one little tweet by the Commander himself), and the US is determined to seek a peaceful outcome without further escalation.

Iran, however, is not content with the US posture and has vowed all sorts of biblical-level destruction on the satans that would attack them. In fact, Iran had already stepped up its bombing of Israel, as expected. Now the world awaits Iran’s next move–it expects one.

I have been monitoring markets since futures opened yesterday afternoon. Markets have had many hours now to digest the situation. The single most discussed risk is the closure of the Strait of Hormuz. It is not new to you because you read my post on June 13th. 😉 That said, wherever you see markets right now, is already factoring in some sort of Iranian response which likely includes some disruption to Hormuz Strait shipping.

Let’s look at that quickly. The Strait of Hormuz is a known choke point where the Persian Gulf meets the Gulf of Oman opening up to the Arabian Sea. The issue at hand is that the Strait of Hormuz is only 20 miles wide making it a likely target to upset shipping. Shipping which includes 20% of the world’s crude supply.

If your dog sat on your television remote yesterday, your TV would likely land on a station that had some talking head expelling information about the Strait of Hormuz and the implication of shutting it down. It’s old news, but it is important nonetheless. What would give us the idea that Iran would try to choke the strait? Well, its parliament allegedly approved the tactic yesterday. Oh, and I forgot to tell you, they have done it–or attempted to do it–in the past… a couple of times. The most serious threat came in 1984 - 1988 in what has been dubbed The Tanker War. During that period over 400 ships were attacked in the strait. Missiles, fast boats, and naval mines were all part of the offensive.

So what happened to the markets during that period? Well, stocks actually had a pretty good run up until the Black Monday crash in 1987. Crude oil and Hormuz had nothing to do with it. You would have to go all the way out to 1990 to see a crude-related market decline. That was the year that Iraq invaded Kuwait in the first gulf war. The war certainly contributed to the decline, however the US economy was already on weak footing leading up to that year. Crude prices more than doubled by the fall of that year, spiking inflation fears. However, prices retreated soon after almost back to pre-war levels.

So, that brings me back to my original question. Will the US’s action over the weekend result in similar declines if a broader conflict ensues? Unfortunately, it is difficult to compare economic conditions. We do know that inflation is very much a concern today as it was back in 1990. Spikes in energy could certainly ignite further fears causing stock declines.

But the question remains, what will happen in the Strait of Hormuz. If Iran decides to proceed with a shutdown of the strait, it will do so using mines, fast boats, missiles, and drones. As Israel enjoys air superiority over Iran, US along with other coalition forces which may include gulf states will enter the theater to minimize the threat. It is therefore unlikely that Iran can actually close down all 4 shipping lanes through the straits. Additionally, mines will quickly be cleared and naval escorts will strive to keep order. Now to be clear, fear and slowdowns will hamper movements and likely come at a cost, albeit not a severe one. Further any attempts to completely choke off the strait will likely be short lived.

In short, an escalation to “severe” threat is possible but not probable. If the situation escalates, stocks along with commodities will certainly react, though only in the short run. Stocks as a result may continue to be volatile, but the long run, positive trend will persist. Below, I will share the same chart-completely unmodified- that I created and shared on the 13th. It is still valid!

Now, what did I tell the press on Saturday night? I pointed out that Hormuz was indeed the wildcard risk, but ultimately the US move would be positive for stocks. The risk of escalation was already present and accounted for last week. The attack was making an unknown known. Markets hate unknowns. Is the threat of an Iranian response a new unknown? If it includes the Strait of Hormuz… well, if you have been paying attention, really, no.

FRIDAY’S MARKETS

Stocks struggled to stay afloat on Friday as traders considered the growing threat of further conflict in Iran. It was just another unknown atop a pile of existing ones that have been vexing the markets keeping the bulls from breaking out.

.png)