.png)

AI isn’t killing software. It’s exposing weak business models. Here’s what investors are missing.

KEY TAKEAWAYS

-

The recent software selloff reflects broad-brush panic rather than company-specific analysis. AI jitters have become a lazy narrative that ignores structural differences across business models.

-

Enterprise software leaders like Microsoft, Adobe, Salesforce, and Intuit possess durable moats in distribution, data, and workflow integration. AI is more likely to be embedded into these ecosystems than to displace them outright.

-

Snowflake represents a more nuanced case where competitive dynamics are shifting as cloud providers bundle AI capabilities. The risk lies in margin compression and pricing pressure, not extinction.

-

The real vulnerability sits in commoditized digital labor platforms and single-purpose output businesses. When AI becomes a direct substitute rather than an enhancement, disruption risk increases materially.

-

Private credit exposure adds another layer of complexity. If AI weakens leveraged operating companies, risk migrates upstream into credit vehicles offering elevated yields.

MY HOT TAKES

-

AI is accelerating capitalism rather than ending it. Weak models and weak management teams will be exposed faster than in prior technological shifts.

-

Not all software should be treated equally. Durable moats tied to data ownership, switching costs, and regulatory integration remain powerful defenses.

-

Margin pressure and stack consolidation will redefine where value accrues in the AI ecosystem. Toll collectors may change, but the castle still stands.

-

Headline-driven fear is creating mispricings across high-quality enterprises. Volatility is punishing strength and fragility simultaneously.

-

Higher yield always signals higher risk. When AI compresses operating margins, that pressure flows directly into credit structures funded at optimistic valuations.

-

You can quote me: “AI isn’t ending capitalism--it’s accelerating it.”

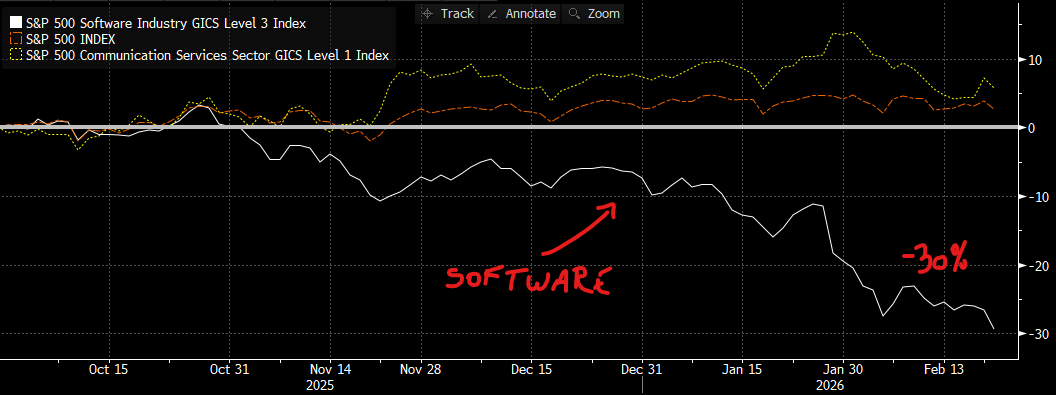

More babies. Stop and listen. Can you hear that? That is the cry of 1000 babies who have been thrown out with the bathwater. It is becoming common practice these days, and yesterday’s broader market rout is a clear example of this. Yesterday, I commented to a journalist that jingles like “AI jitters” and, now “software jitters” have become common amongst traders. We keep reading things like, “markets declined due to [some sort of AI-born] jitters.” Jitters? Really? Pay attention now, because you don’t want to get this one wrong. Some explanation is necessary. Let’s dive right in. Start with the following chart and keep reading.

This chart compares the performance of the S&P 500, the S&P 500 Software Index, and the S&P Communications Services Index from Q4 of last year through yesterday. Without reading my annotation, I am sure that you know that the white line represents the software index which was down by just about -30% compared to the S&P 500 which was up by -2.23% over that time period. If you have been paying attention to the mainstream media, skimming headlines, or even attending cocktail parties, you probably think you have the answer to why this has happened. You may even have fallen prey to the fear and sold some of your babies and accentuated the pullback. I can’t say that I blame you. AI is powerful, and you have probably dabbled with it and realized quite fast that it can be a real gamechanger. So, when someone gets on TV and says that software is getting beaten up because AI will obsolete all those companies, it strikes a chord. But, my friends, we are smarter than that.

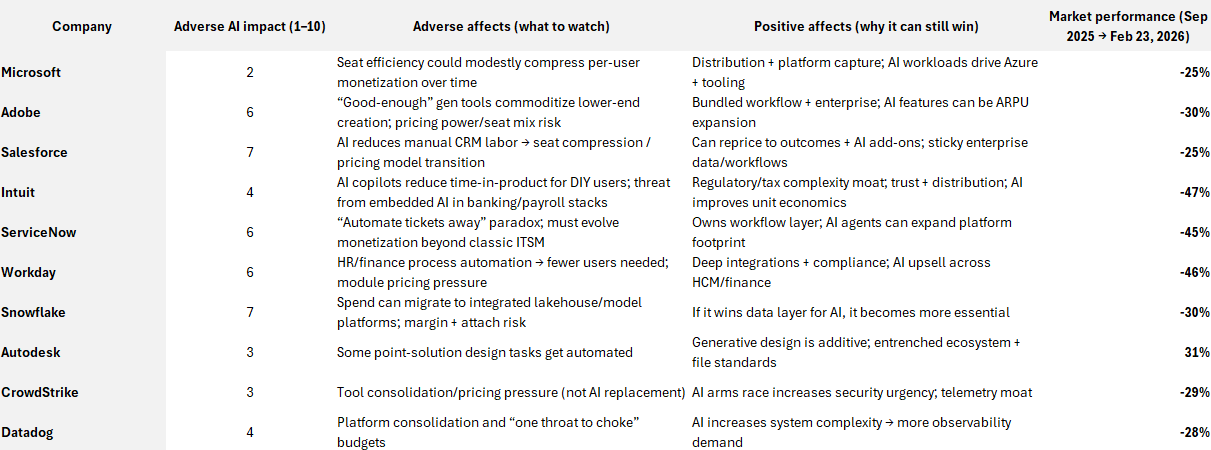

Let’s start with some of the names in that software index that lost -30% over the past few months. Some of the top-weighted companies in the software index are Microsoft, Adobe, Salesforce, Intuit, ServiceNow, Workday, Snowflake, Autodesk, Crowdstrike, and Datadog. I am sure that you know most of these companies and probably even own a few of them. Now, it is clear that AI will impact each one of those names on the list. For some, AI will enhance their business, while for others, it will certainly require strategic course corrections.

I put all these companies in the simple table that follows. I show you the potential level of adverse impact that AI may have on the company (1 - 10, 1 being the least), what those impacts may be, and also the potentially positive impacts AI will have on those companies. Have a quick look and keep reading.

Now, take a beat and actually think about what you just saw in that table. Does it really make sense that Microsoft, Adobe, Salesforce, Intuit, ServiceNow, Workday, Snowflake, Autodesk, CrowdStrike, and Datadog should all be painted with the same broad, sloppy brush labeled “AI victim”? Of course not.

AI is not a meteor. It is electricity. ⚡

Electricity did not destroy factories. It destroyed inefficient factories that placed their bets on horsepower and steam. Personal computers did not eliminate accountants. It eliminated those who insisted on using ink and ledger paper while competitors embraced spreadsheets and databases. AI is following that same path–only faster. Much faster.

Let’s start with one of the babies that looks the most blighted: Adobe. Adobe has been treated like it is roadkill on the side of the AI highway. Generative image tools pop up, and suddenly the narrative becomes, “Why pay for Photoshop?” That sounds clever at a cocktail party. It sounds less clever when you actually understand how creative workflows function inside enterprises. Adobe doesn’t just sell image generation. It sells standards. It sells collaboration. It sells integration across creative, marketing, and publishing pipelines. It sells workflows.

Indeed, AI commoditizes some low-end creation. Yes, hobbyists may churn. But professionals and enterprises don’t run their brand infrastructure on novelty tools. They run it on platforms that integrate deeply across teams. If anything, the companies that embed AI into existing workflows, rather than stand outside them, are in a stronger position long term.

That is precisely what I mean when I say some babies are being thrown out. Now let’s talk about one that deserves careful scrutiny: Snowflake. To be very clear, Snowflake is not dying and it is not some outdated warehouse stuck in the past. But it does sit in a more delicate position as AI reshapes the data world. The big cloud providers (e.g. Microsoft, Amazon, Alphabet, etc.) are bundling storage, compute, model hosting, databases, and orchestration into unified AI platforms. When everything is packaged together, it becomes harder for any single layer to defend premium pricing. Snowflake makes money from consumption across its data platform and is building AI capabilities of its own, but competition around that layer is intensifying. The risk is not that Snowflake disappears. The risk is that as the stack consolidates, margins and pricing power come under pressure.

Made simply, Snowflake once stood guard at the main gate to the structured data castle. If you wanted access to the kingdom’s data, you passed through that door. AI, however, has expanded the castle walls and added new gates–model layers, orchestration layers, integrated cloud stacks. The castle still stands. The question is who collects the toll at each entrance. Snowflake is fighting to remain one of those toll collectors, but it no longer controls the only gate. That’s not panic. That’s structural awareness. I know that this is difficult to understand, but it is absolutely critical to focus on this if you want to invest in the space effectively.

And here’s where investors get sloppy.

Lately, investors hear “software” and assume “AI kills it.” But the real roadkill is not in the classic enterprise software names. It is in the Communication Services and marketplace layer–the single-purpose output businesses that are not in that list above; they may not even technically be “software” companies. I am talking about companies like Chegg or Fiverr. Businesses that monetize answers, routine tasks, or commoditized digital labor. When the product is “information retrieval” or “basic content generation,” AI is not an enhancement. It is a substitute.

Those, my friends, are the models we must be weary of. The difference is subtle but critical. Salesforce owns customer relationships. That data moat matters. Intuit owns financial data and regulatory workflows. That moat matters even more. When I wrote a few days ago that companies with strong data and customer moats will likely win, this is what I meant. AI doesn’t eliminate moats. It changes their composition.

The key question is always this: what does the company actually own? Does it own distribution? Does it own proprietary data? Does it own switching costs? Does it own regulatory integration? Or does it simply own a digital interface that can be replicated by a smart kid in her mom’s basement?

Management quality is always absolutely critical but now matters more than ever. The better-run firms will not resist AI. They will embed it. They will reprice it. They will pivot. They will shrink legacy cost centers and expand high-margin AI layers. This transition process is not new. We have seen it in every technological revolution. What is new is the speed. AI compresses the adaptation cycle. Weak management teams get exposed faster. Strong teams create leverage faster.

I have written repeatedly about hot private money chasing too few good deals. When capital floods into private credit or opportunistic lending structures, underwriting standards drift. Valuations get optimistic. Transparency declines. And when the cycle turns, everyone acts surprised.

Surprised? I hope not. If you chase yield, you inherit risk.

And let’s be precise about yesterday’s Citrini chatter. The so-called “bombshell” was not really about retail investors recklessly buying private credit funds–that is already swirling around the markets. It was more about the AI shock running through the underlying companies that many of these vehicles have financed. That is a critical distinction. The structure is not inherently flawed. The fragility lies in what has been financed and how durable those business models are in an AI-accelerated world.

If AI compresses margins, automates workflows, lowers barriers to entry, or shifts competitive dynamics, then highly levered companies feel that pressure first. And if private credit funded those companies at optimistic assumptions, the risk flows upstream. That is not scandal. That is math. Risk in the operating company becomes risk in the credit and eventually risk for the investor reaching for that higher yield.

Unfortunately, it is difficult for investors in private credit BDCs to know precisely what some of these vehicles own. Disclosure can be murky. Valuations can be opaque. That makes diligence harder, not optional. But one rule remains eternal: if the yield is meaningfully above market, the underlying asset carries meaningful risk. That is not cynicism. That is finance!

And this ties directly back to the broader AI conversation. AI will expose weak business models. It will expose aggressive capital structures. It will expose firms that relied on financial engineering rather than durable competitive advantage. It will expose those who mistook cheap capital for real moat. That doesn’t mean the sky is falling. It means the market is repricing risk in light of a faster competitive cycle.

Take a breath, because there is a positive note here. A big one. AI is creating one of the largest opportunity sets of our investing lifetimes. It is rewiring supply chains, productivity, service delivery, analytics, healthcare diagnostics, legal workflows, software development, and manufacturing. The long-term opportunity is clear, but the short term will be tempestuous.

Transitions are never smooth. Proliferation phases are messy. Capital overshoots. Narratives get exaggerated. Good companies get punished alongside fragile ones. Separating those babies from the bathwater is not easy work, but it is THE work.

You cannot outsource that judgment to headlines. You cannot rely on “AI jitters” as an explanation. You must understand the business model. You must understand the moat. You must understand what management is doing to evolve.

AI is not ending capitalism, but rather, it is accelerating it.

Those who adapt will thrive. Those who resist will fade. And those who cannot tell the difference will keep throwing babies into the street every time volatility knocks. If long-term success is the goal, it is time to get very, very good at knowing which cry matters, and which one is just noise.

YESTERDAY’S MARKETS

Stocks got knocked off their feet with deep declines yesterday after enduring a blizzard of negativity. Stocks started on uneven footing as the administration reacted to last Friday’s SCOTUS ruling against tariffs. Tariff continuation was priced in, but perhaps not across the board ones at 15%--tariff uncertainty returns. A report highlighting potentially negative risks posed by AI to virtually everything collided with the prevailing “jitters” to cause stocks to lose altitude. Jitters beget jitters.

NEXT UP

-

ADP NER Pulse (Feb 7th) came in at 12.75k, an increase over last week’s 11.5k jobs adds.

-

FHFA House Price Index (December) may have increased by 0.3% after climbing by 0.6 in the prior period.

-

Conference Board Consumer Confidence (February) probably increased to 87.1 from 84.5.

-

Fed speakers today: Goolsbee, Collins, Bostic, Wall, Cook, and Barkin.

-

Important earnings today: Keurig Dr Pepper, Home Depot, Constellation Energy, Digital Ocean, American Tower, NRG, Cava Group, Mosaic, Lucid, Realty Income Trust, HP Inc, Workday, goDaddy, First Solar, and CoStar.